A new generation of clean energy begins in the United States. As the Inflation Reduction Act of 2022 (IRA) becomes law, we embark on new and historic opportunities for developers, investors, and renewable energy buyers. Numerous analyses demonstrate the clean energy and climate provisions of the IRA will spur economy-wide greenhouse gas emission reductions of 40 percent while beginning to reshore critical manufacturing supply chains. This will allow corporate leaders to accelerate clean energy investments and to make more impactful energy procurement decisions as the IRA begins the process of addressing historical energy inequities in communities across America.

Additionally, the IRA will spur new technological growth which will lead to new clean energy resources and increased project availability for energy buyers across the US. Energy Innovation also found that the IRA could create up to 1.5 million jobs by 2030. Underpinning the success of the IRA is the need to scale the renewable energy sector. Wood Mackenzie estimates that, at a minimum, the IRA will lead to 67% more solar.

What’s in a Name?

In our last CEO letter, we highlighted the threat that inflation poses to the renewable energy industry while noting the deflationary potential of clean energy. The aptly named Inflation Reduction Act’s monumental investments in clean energy should have a long-term deflationary impact.

What’s in the Law?

Clean Energy Tax Credits

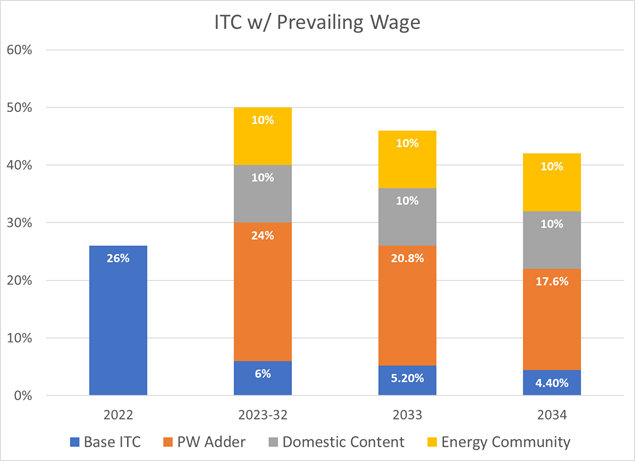

Among other credits, the clean energy tax credits in the IRA maintain the historic standalone solar ITC until 2025 when the credit shifts to technology-neutral. Essentially, after 2025 the IRA tax credits incentivize any method of generating electricity without emitting carbon dioxide (CO2). This includes stand-alone energy storage, clean hydrogen, and advanced and existing nuclear, as well as domestic manufacturing. Additionally, credit recipients, including solar, now have the option to select either the investment tax credit (ITC) or production tax credit (PTC). We anticipate that most solar operators will continue to prefer the ITC, at least in the initial years. The below illustrates the base ITC and adders available to larger solar projects meeting labor requirements (additional incentives are available for smaller projects, including the ability to consider interconnection costs in calculating total project cost eligible for the ITC). These credits will begin to phase out the later of 2032 or when the electric power sector emits 75 percent less CO2 than 2022 levels. This will for the first time directly connect clean energy credits to decarbonization goal, and ensure they are available to achieve it.

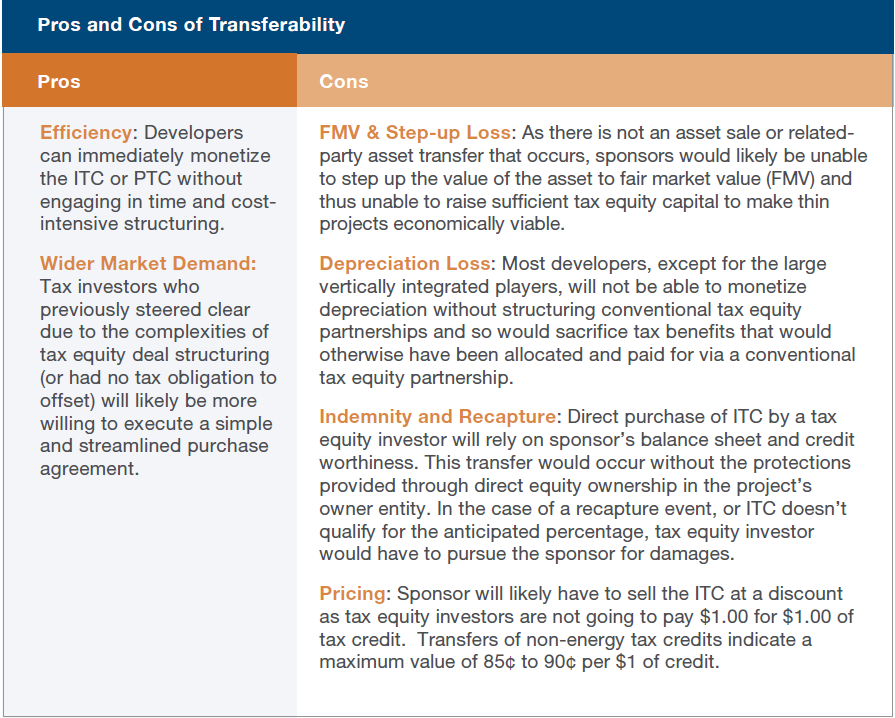

Important to note that the IRA sets the base ITC at siAlthough we expect that the IRA’s new direct-pay and transferability options will allow new participants without tax obligations, such as electric cooperatives and municipal utilities, to construct renewables, we do not expect the new options to slow appetite for traditional structured tax equity transactions. To begin with, we expect guidance and initial demonstration of the new options to take at least a year, advantaging traditional tax equity investments in the near term. But even over the longer term, we expect structured tax equity financing will remain more attractive to corporate partners because of its lower recapture risk, its ability to monetize depreciation, and the opportunity it provides for projects to be valued at fair market value rather than cost. The chart below provides a high-level overview of the advantages and disadvantages of transferability versus structuring from a sponsor’s perspective.

Beyond the changes in methodology for investors to acquire tax credits, the IRA allows solar projects to elect Production Tax Credits (PTC) instead. This opens the possibility of structuring a PTC investment similar to the PAYGO financing tax equity structure that exists in the wind segment of the market today. Within the solar space, this could provide additional benefit in geographies with high yields and where production is highly predictable.

Implications for Developers

We expect a limited positive impact on current projects given that the 2022 ITC rate has now increased to 30 percent from the expected 26 percent without triggering labor requirements. We expect this 30 percent to extend into 2023 and for 60 days after the IRS issues new guidance, giving near-term projects an unexpected boost. In addition, the new adders available for projects in fossil fuel transition communities “energy communities” and for projects incorporating domestic content will drive needed investment in both. The

Broad Tax Changes that

IRA seeks to drive clean investment in “energy communities, which may be thought of as energy transition communities – communities that have borne the brunt of fossil fuel usage and should not be left behind in the shift to clean energy. Per the IRA, energy communities include:

- Brownfield sites,

- Areas with high historical fossil fuel employment and currently high unemployment, and

- Areas where coal mines and/or coal-fired power plants have closed.

Thus, a strong financial incentive for projects in energy communities will allow them to continue powering America, but with new access to clean energy resources and funding. In addition to the clean energy and climate benefits, the IRA’s investment in energy communities will have untold public health benefits for communities that have been disproportionately impacted for too long.

Clean Energy Tax Credits

Among other credits, the clean energy tax credits in the IRA maintain the historic standalone solar ITC until 2025 when the credit shifts to technology-neutral. Essentially, after 2025 the IRA tax credits incentivize any method of generating electricity without emitting carbon dioxide (CO2). This includes stand-alone energy storage, clean hydrogen, and advanced and existing nuclear, as well as domestic manufacturing. Additionally, credit recipients, including solar, now have the option to select either the investment tax credit (ITC) or production tax credit (PTC). We anticipate that most solar operators will continue to prefer the ITC, at least in the initial years. The below illustrates the base ITC and adders available to larger solar projects meeting labor requirements (additional incentives are available for smaller projects, including the ability to consider interconnection costs in calculating total project cost eligible for the ITC). These credits will begin to phase out the later of 2032 or when the electric power sector emits 75 percent less CO2 than 2022 levels. This will for the first time directly connect clean energy credits to decarbonization goal, and ensure they are available to achieve it.

Important to note that the IRA sets the base ITC at six percent if new labor conditions are not met, but allows for a step-up to 30 percent if labor conditions are met (the PTC is similarly structured). In order to receive the full ITC (or PTC), prevailing-wage labor requirements must be met for all projects over one megawatt (MW). This includes:

- Payment of prevailing wages during construction, as well as for labor on repairs or alterations during the five-year recapture period on the ITC (for projects over one MW).

- Use of sufficient apprenticeship ratios, unless demonstrably unavailable.

- Additive ITC bonuses would be available for sufficient use of domestic content as well as construction in an energy community. At 10 percent each, a 50 percent ITC is possible for projects that meet both additional criteria. For smaller projects, an additional 10–20 percent is available for solar projects located in certain low-income communities, low-income residential buildings, or on tribal land.

- Transmission upgrades would be considered qualifying property for the calculation of the ITC when part of a project under five MW.

Additionally, for the first time the IRA extends “direct pay” of tax credits to non-profit entities for all resource types and for a limited time to all entities for new categories, such as carbon capture and storage (CCS). Direct pay means that qualifying entities may elect to receive a direct payment of the value of the credit, eliminating the need for participation by an investor with a sufficient tax obligation to monetize them. Entities not eligible for direct pay, including for-profit businesses, are allowed a one-time transfer of each year’s eligible credits to an unrelated taxpayer. We will continue to assess the pros and cons of the new transferability provisions as compared to traditional tax equity financing. Transferability will be effective in early 2023, although forthcoming IRS guidance is necessary to answer questions about how it will work.

Broad Tax Changes that Affect Solar Financing

Several general tax provisions have implications for clean energy financing, most notably the new rules regarding calculation of corporate taxes. For taxable years beginning after 2022, the IRA will apply an alternative minimum tax to C-corporations that have an average annual adjusted financial statement income (i.e., “book” income) for any three-year period in excess of $1 billion. The IRA does not change existing depreciation schedules, but bonus depreciation benefits are slated to phase out between 2023 and 2026, which may have longer term impacts on project finance, as discussed further below.

What’s Next?

What is clearer now than ever before is that clean energy will drive domestic climate action and provide new opportunities for renewable energy growth, procurement, and investment. President Biden signed the IRA on August 16, 2022, and now it heads to the Internal Revenue Service (IRS) for implementation and guidance. While the IRA provides a domestic path to begin building a better tomorrow, it is now on the shoulders of the renewable energy community to execute on the tasks ahead of us and to ensure the future we create is one that benefits all.